By: Ignacio Barros C.

Introduction.-

In recent times, corporate governance has become a much talked about and controversial topic, both in the popular and business press. Newspapers and newscasts frequently feature detailed accounts of corporate fraud, accounting scandals, insider trading, overcompensation of certain officials, and other such organizational failures, many of which end in lawsuits, resignations, and bankruptcies. These business stories, many of them sinister, range from the shocking, such as the Enron case and its sophisticated use of “special purpose” entities and aggressive accounting to disguise its true financial condition, all of course to the detriment of its shareholders , even closer cases in Latin America such as those of HSBC in Mexico, Inverlink in Chile and, of course, that of Odebrecht, which is without a doubt the biggest case of corporate corruption in the history of this region. Even if we review Europe we will also find cases such as those of Parmalat, Royal Bank of Scotland, Shell and Siemens, which have been plagued by scandals related to failures in the supervision of their senior management.

But what is the root cause of these failures? Reports agree that these companies suffered from a failure in their corporate governance. What, then, is corporate governance? As the book Corporate Governance Matters, by the authors Larcker and Tayan, points out, in theory, the need for corporate governance lies in the fact that when there is a separation between the ownership of a company and its management, that is, when the shareholders are not the same managers, the possibility arises that some executives, more interested in themselves than in the well-being of the company as a whole, take actions that benefit them at the expense of shareholders and other interested parties, who assume the cost of said actions. This scenario is generally known as the agency problem, and the costs resulting from this problem are called agency costs. To reduce these costs, some type of control or monitoring system must be implemented in the organization. That system of checks and balances is called corporate governance.

Behavioral psychology and other social sciences have provided us with evidence that people are, in general, selfish and tend to put our own interests before those of others. In his famous book The Economic Approach to Human Behavior, Gary Becker (1976) applies his theory of rational self-interest to economics to explain human tendencies, including the tendency to commit crime or fraud. He shows that, in a wide variety of settings, people decide to take inappropriate actions to benefit themselves if they believe that they will go undetected and thus avoid the cost of punishment. Society then establishes control mechanisms to dissuade this type of behavior, by increasing the probability of detection and changing the risk-gain balance so that the expected reward of the offense decreases.

Elements that make up corporate governance.-

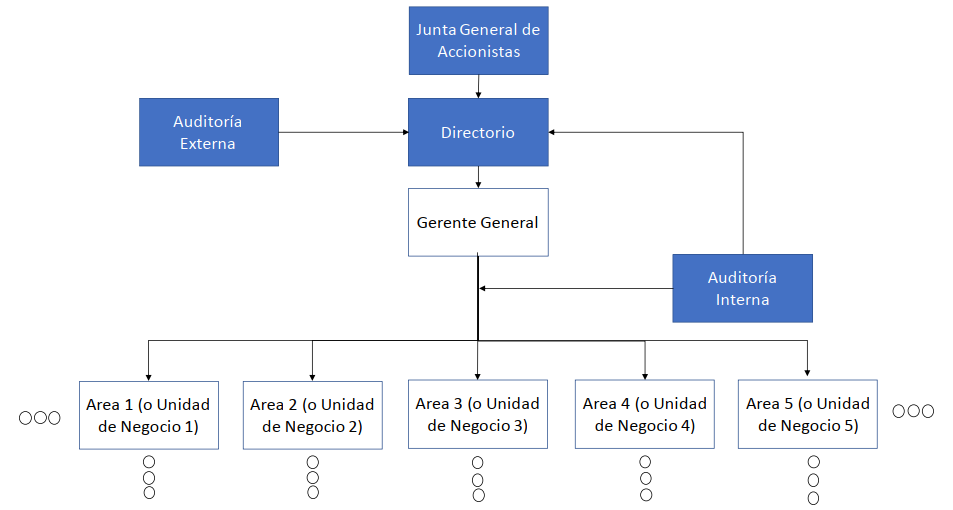

The experience we have at Synergos advising companies to implement their governance structure tells us that there are four elements that are crucial and must be clearly and formally defined. These are the general meeting of shareholders, the board of directors, the external audit and the internal audit. We believe that the presence of these four control bodies -or pillars- of corporate governance apply to both medium and large public and private companies. Graphically:

The general meeting of shareholders is the supreme control body, and basically has three functions:

- Carry out the final approval of the financial statements (preliminary approval is held by the board of directors)

- Decide the distribution of profits based on the approved financial statements

- Appoint and remove directors

They normally meet once a year since the three functions just described have an annual frequency.

The board of directors is the second control body and is the main actor of corporate governance, moreover, for many authors the mere implementation of the board of directors is synonymous with the implementation of corporate governance. This article is not intended to be an exhaustive treatise on what a directory implies, far from it, but what we do want to highlight is that its two main functions should be:

- Advise and

- Supervise senior management

Although these two responsibilities are linked in many ways, they have fundamentally different approaches. In its advisory role, the board guides management and provides advice on the strategic and operational direction of the company. It focuses primarily on those decisions that correctly balance risk and reward. In its supervisory role, by contrast, the board is expected to oversee management and ensure that it acts diligently in the interests of shareholders.

Some key success factors that we have seen implemented in highly effective directories are:

- Adequate and complementary profiles of the members, in terms of expertise, gender and age

- Independence to avoid conflicts of interest

- Odd number of members to achieve a simple majority in voting

We have seen boards in which the chairman of the board (the chairman) is also the CEO of the company, and boards in which he is not. To cite an example, in 53% of the companies that make up the US S&P 500 both positions fall to the same person. In other words, practically half of these companies consider that it is appropriate and the other half thinks the opposite. There is no consensus on this point. We see pros and cons in both positions.

Another interesting fact is that the time that an average director dedicates to his management tasks in a large company -or corporation- both in Latin America and in the US, is approximately 20 hours per month.

The External Audit is the third control body and its importance does not withstand analysis. The need for a competent and impartial third-party entity to audit the financial statements and provide shareholders with peace of mind that the figures reported by senior management are correct is evident. However, we have seen cases in which this pillar of corporate governance has been violated by bad practices. In June 2002, Arthur Andersen, until then one of the most prestigious auditing companies in the world, was found guilty of obstruction of justice for destroying Enron-related documents, marking the beginning of the end for the auditing company founded in 1913. Having said this, the fact that this pillar is potentially vulnerable does not deny that it is fundamental and that it must be present in every structure of government. The way to mitigate its vulnerability is the same as to mitigate the vulnerability of any of the other three pillars: the joint work of the four control bodies is the strength of the model. The probability that all four pillars are violated is significantly less than that one or two are.

Finally, the Internal Audit is the fourth control body and is often the most relegated pillar. In fact, in many organizations we see that the central functions of internal auditing, such as risk mitigation, asset control, review of the efficiency of certain critical internal processes and compliance with the objectives and goals of the organization, they fall into different areas, thus losing the centralizing force of this area. On the other hand, we have seen successful cases where the management information system through indicators is the responsibility of this area, and said indicators are reported monthly to the board of directors. In this way, a double reporting line is generated for the Internal Audit, one to the CEO and the other to the board of directors, thus eliminating the possible bias that the general management could give to this area, reducing its impartiality.

Final words.-

It is important to emphasize that not everything has been said in terms of corporate governance. If one reads the most reputable books and articles on the subject, one will see that there are discrepancies on each point, that the bulk of the statistical studies carried out do not show conclusive correlations, and that the implementation and scope of each government structure depend a lot on cultural aspects. of each country and each organization. We believe that careful empirical studies should continue to be done to better understand what works and what doesn’t so that changes can be made cost-effectively. We have no doubt that the implementation of a good governance system is essential for the sustained success of an organization. The fundamental challenge is to understand when and how it should be implemented. That’s where the magic is.